Category: Management

Most of the quotes we discuss in The Entrepreneur’s Weekly Nietzsche we found by reading his work, but a few are well-known lines that you may have heard before. This is one, used in our chapter “Monsters”:

He who fights with monsters should be careful lest he thereby become a monster. And if thou gaze long into an abyss, the abyss will also gaze into thee.

The quote leads quickly to questions of ethics. In the chapter, we discuss the fact that we each have our own views of what constitutes ethical or unethical behavior in business. It is a line-drawing game – there is no reference that everyone agrees on. The choices have both short- and long-term consequences for both the success of your business and for your own reputation. Further, once you choose an ethical approach, it becomes entrenched in your organization and is difficult to change.

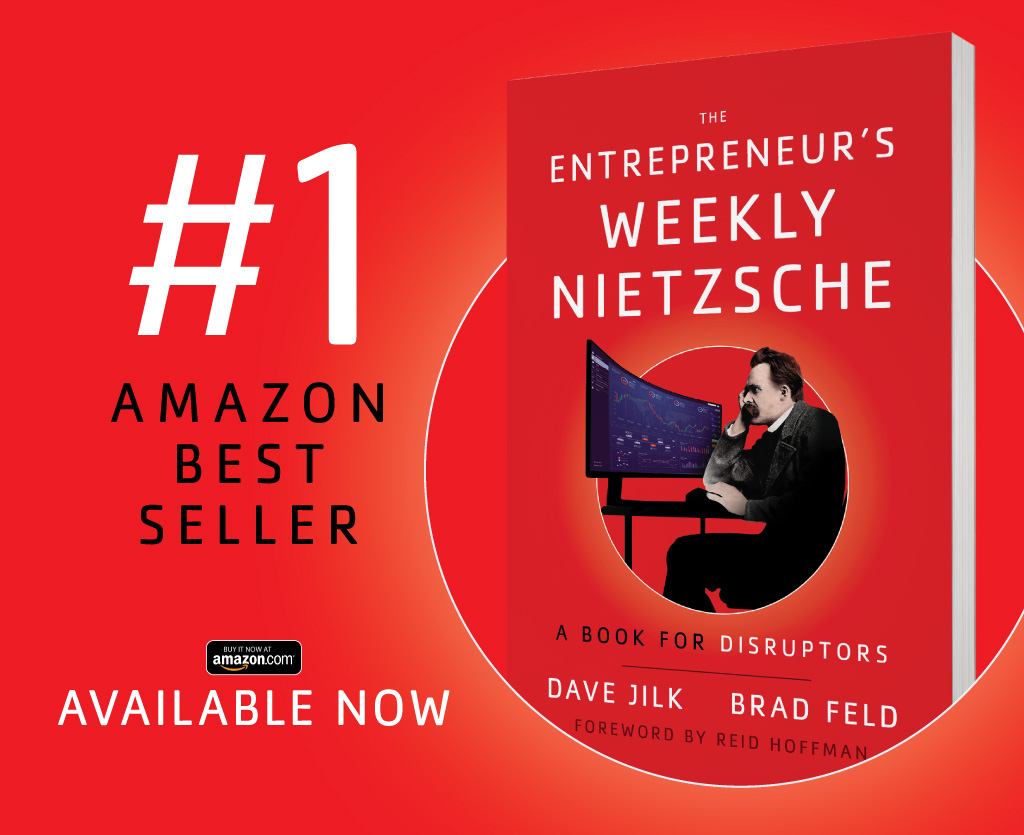

These questions arise pretty much every day in business. It came up for us today with our own book promotion. Our publisher was excited that we had achieved “#1 Amazon Best Seller” status in a couple of categories and produced the graphic below for promotion. The thing is, the categories were things like “Existentialism” and “Philosophy Reference” where overall sales are lower – they are applicable to the book as categories, but not really our target market (for the record, the book is selling nicely in “Entrepreneurial Management”, where it was briefly #2.)

The question is, should we use it, or is it misleading and dishonest?

We expect that most of you will say that of course we should use it, because strictly speaking it is true, and it will help sell the book. A few might agree that it is a little uncomfortable, perhaps preferring that the language be changed a little. Others will say that the question is overthinking a simple thing, and why should one even worry about it?

This is indeed a simple example, and in isolation this is overthinking. It’s not going to show up as a scandal on the front page of the New York Times. But if you never examine such questions, the pressure of competition and the temptation of promotion can be an abyss that gazes into you. Eventually you may find yourself, or people in your organization, saying things like “A lot of people are telling me…” (where have you heard that before?) Such statements are strictly true, depending on one’s interpretation of “a lot.” How is this marketing image different?

Our book asks you to think harder about questions like this, and many others that may not have such an explicitly ethical component.

As another example, Dave wrote this post after a quick back and forth this morning about the issue on email while I was on another call. I read it, make a few light edits, and posted it. One approach would be to just post this. Instead, I asked Dave how he wanted it posted since he was the primary author. As we went back and forth in email (his answer: “Either say we both wrote it or credit me, either is fine. I’d lean toward the first.”) just reinforced our own alignment, while being a nice self-referential example.

And … we both just looked and the book is currently selling at #1 in both “Business Management Science” and “Business Technology Innovation.” Ahhh, that feels better.

Each morning during the week, after morning coffee together, Amy says, “Ok, time to go eat my frogs.” She’s usually told me about the one or two or three frogs she has for the day, and her statement is a rhythmic part of our morning.

Yesterday, I asked her where that phrase came from. She pointed me at Eat That Frog!: 21 Great Ways to Stop Procrastinating and Get More Done in Less Time, a productivity book by Brian Tracey that she read a few years ago. (Note, a blog reader sourced the original quote to Mark Twain.)

While I haven’t read the book, we are using the phrase a little differently than the motivating language on the Amazon book website.

It’s time to stop procrastinating and get more of the important things done! After all, successful people don’t try to do everything. They focus on their most important tasks and get those done. They eat their frogs.

There’s an old saying that if the first thing you do each morning is eat a live frog, you’ll have the satisfaction of knowing you’re done with the worst thing you’ll have to do all day. For Tracy, eating a frog is a metaphor for tackling your most challenging task—but also the one that can have the greatest positive impact on your life.

Stop procrastinating is correct, but it’s mostly aimed at a task that is difficult for some reason. And, what is difficult for Amy is different than what is difficult for me, and vice versa.

If you recall my post, Something New Is Fucked Up In My World Every Day, you will see the link between Milarepa and eating frogs, even if demons aren’t involved.

Between Monday and Friday, my work as a VC includes an endless number of difficult things. I say no all day long. I give people news or feedback they don’t want to hear. I deal with conflict, angry and frustrated people, and strange situations that cause emotional pain. Often the pain is from exogenous factors that dramatically influence things, but which we have no control over.

And yes, Something New Is Fucked Up In My World Every Day. I can’t predict when it will show up, but it’s often late enough in the day that I can’t solve it before I stop working. And many of these things extend over many days and have numerous frogs contained within them.

I used to procrastinate on things I didn’t want to deal with. In my 20s and 30s, I’d carry them around with me, waiting for the right time to address them. By the time I hit my 40s, I had stopped doing this with most things and just dealt with whatever came up head-on. When I found myself procrastinating on something difficult, I realized I was avoidant, often passive avoidant, and would go deeper on why I was procrastinating which often helped me understand the thing better. Occasionally, I’d continue to be avoidant, sometimes unconsciously, but the demons eventually showed up, and I had to embrace the lessons of Milarepa to get rid of them.

I still procrastinate, but it’s on things that either don’t have a deadline or things that I’m looking forward to doing. If you’ve written a book with me, you understand this statement well (Ian, I’m thinking of you.)

The frogs? I eat them whenever they show up or first thing in the morning. And, even though I’m a vegetarian, I’ve come to get satisfaction from eating my virtual frogs. So that’s another life lesson from Amy.

My partner Chris Moody recently sent around a note on a concept he refers to as Leader Leverage. I encourage every CEO to read and consider it. His rant follows.

Many of you are probably tired of hearing me rant about some form of what I often refer to as “leader leverage”. If you’ve been lucky enough to avoid these rants, the quick summary is that your biggest lever as a board member is the CEO and your biggest lever as CEO is your direct reports. I learned this lesson the hard way running a very decentralized business with 70 offices in 17 countries at Aquent.

A critical learning about a company’s leadership is whether or not employees trust and respect their senior-most manager. Yet, asking this question directly often doesn’t get a great answer. However, asking it indirectly can be magical.

Using an NPS approach, the example below asks the question, “The company is in a position to really succeed over the next three years.” The different answers are by department.

The average employee believes the Company is in a position to succeed over the next three years. The exception is the employees in one particular department (the red box) who all believe the company is completely fucked. This perfectly illustrates the point that the collateral damage of having a bad leader goes far beyond that leader’s ability to perform their technical job because a bad leader will usually poison a team’s perception of the entire company.

We’ve known for a long time that we needed a new leader in that department for the Company. However, we’ve always viewed the issue with the current leader to be an issue around technical skills. It turns out the ramifications of not having a leader that people can trust and respect goes far deeper.

At Aquent, we found similar results around crazy specific things like compensation where people would go from feeling grossly under-compensated to feeling like they were compensated fairly simply because we made a change in the leader of their market.

If you found this useful and want more of Moody on topics like this, I encourage you to go watch his vlog Venture Kills. For example:

I used to love the Matrix’s Red Pill / Blue Pill metaphor and still use it occasionally to try to make a point around dealing with reality in an entrepreneurial context. Several years ago, I became deeply bummed out about how this metaphor was being used in politics and gender equity situations. It’s gotten worse since then, and I find many of the cases it is used in and the people who use it reprehensible, so I don’t use it much anymore.

However, I used it today for a company that is doing well and has exceptional strengths and some fundamental weaknesses.

This is true of every company that is doing well.

But it’s hard to deal with reality all the time. When things are going well, leaders (and boards) often avoid dealing with weaknesses. Some board members and investors are great at motivating a CEO to level things up. Others aren’t. Some CEOs want to embrace the challenge of leveling up in areas where they, and the business, are fundamentally weak, even if it’s emotionally and functionally challenging. Others don’t, or their own behavior and wiring get in their way.

There are many points in a company’s life where the CEO and the board can either deal with or deny reality. When dealing with reality, a key factor is embracing the business, team, and individual’s weaknesses and then deciding how to address them. Collectively. With empathy and emotional support for each other.

This isn’t easy. Over the past 30 years, I’ve been in this position many times, often multiple times as a board member in a particular company. These are different than crisis moments, where everything is on the line. It’s often when many things are going well, but there are prominent areas of the business that aren’t keeping up with what’s working.

I’ve never figured out magic words to say as a board member in these moments. Instead, I say what is on my mind, take responsibility for my participation in any weaknesses, dysfunction, or challenges, and focus on where I think we need to put additional energy in improving the business.

This is often an acknowledgment that we need to add a few experienced people to the leadership team. The CEO has to drive this. When the right people are added, notable positive shifts in the weaknesses can happen extremely quickly. But, in the absence of them, the talk generally continues, without action. Reality is not dealt with – just poked around the edges.

One of an effective board’s roles is to speak clearly about the weaknesses and hold the CEO accountable for addressing them. When I am effective as a board member, I do this well. When I’m not, I don’t. I’ve got plenty of cases of both in the last 30 years.

My mantra as a board member is:

“As long as I support the CEO I work for her. If I don’t support her, my job is to do something about that, which is not to replace her, but to try to get back to the place where I support her.”

Ultimately, as a board member and major investor, I can participate in replacing the CEO. While I’d prefer not to do that, I’m not afraid of doing it. But dealing with reality with the existing CEO is much more enjoyable and has generally been a more successful path for me.

All of this is extremely challenging, as it has to do with personal growth in the context of business growth. It’s easier to have entrenched thinking, play out the exact historical patterns that worked or be resistant to addressing whatever the current reality is. It’s compounded by the fact that exogenous factors are constantly changing and often change extremely fast.

The probability of long term success increases with a CEO, a board, and a leadership team is tuned into whatever the current reality is, their strengths and weaknesses, and focus on continually leveling up the weaknesses while continuing to play to their strengths.

If you are a CEO, spend a few minutes today contemplating whether your board is highly effective at helping you grow, scale, and evolve the business. Are you systematically and continuously addressing your weaknesses as an individual, leadership team, and company?

Are you dealing with reality?

In the US, we are currently getting a master class in “how not to lose.”

When I was young, my parents regularly said to me, “Don’t be a sore loser.” I was a serious tennis player between the age of 10 and 14. John McEnroe was my hero, so, not surprisingly, I had a temper on the court. I threw my racket, screamed a lot (mostly at myself), and moped around when I lost.

I also played soccer. For a few years, I was a goalie until one fateful game. I remember it being a big game – whatever our equivalent of a championship or playoff game was. I was a good goalie – quick, pretty fearless, with excellent hand-eye coordination. The game was a tie and went into a penalty kick shootout, which was a particularly cruel thing to do to a bunch of ten-year-olds. I can even remember the name of our team’s star (Scott), who missed his kick. I then missed the save on the next shot from the other team, and they won the game.

I walked off the field sobbing. I’d let my team down. If only I could have saved that goal. Why didn’t Scott make his shot? It was all my fault. I sucked.

My mom put her arm around me and said, “Don’t be a sore loser.” She hugged me. I still remember that.

When I play tennis, I still mutter to myself, but I no longer scream, throw my racket, or swear at the other player. I’ve won a lot in my life, but I’ve also lost many times. And, when I reflect on losing and tennis, I think of the two people who model losing and winning better than anyone I’ve ever seen.

Rafael Nadal and Roger Federer.

Following is an example from the 2017 Australian Open.

Nadal is exhausted from the tournament. And he lost. And yet, grace. Minute 1:45 – 2:00 of the video is delightful.

Winning gracefully is equally powerful. Following is Roger Federer from 2017. Minute 2:15 – 2:30 is beautiful.

This is how you lose. This is how you win. And then you get up the next day and try again.

My post The Future Of Work Is Distributed received some good comments. More interesting was the number of direct emails I received back with detailed information about “remote-first” companies and how they did things.

There was a distinction in some of these emails between “remote-first” and “multiple geographies.” It’s an important nuance, as there is a big difference between a fully distributed workforce (which the blockchain kids refer to as a “decentralized workforce”) and a multi-location workforce.

Almost every company in our portfolio with more than 50 employees either has or is looking at a second (or third, or fourth) location. This is especially true for companies headquartered in Silicon Valley, Seattle, and New York.

While I’ve observed (and experienced) mixed success with second locations being implemented too early, I’ve concluded that this is mostly a function of the company not having a handle on how to deal with a distributed workforce. When the CEO prioritized either distributed or remote work and makes it part of the wiring of how the company operates, it’s effective. When it’s an afterthought, a lifestyle choice, or a reaction to something, it fails.

I’ve found that secondary/tertiary US cities work better than international locations, with the exception of software/hardware engineering locations. Several of our companies have had great success in Eastern Europe and Russia with technical teams. China and India work, but seem to be harder and more hit or miss. Cities in the US that have concentrations of technical, sales, or operational talent, usually because of one specific employer or a highly motivated university nearby, have been surprisingly effective.

The biggest magic trick seems to be the “direct flight.” When it’s a two hour or less direct flight to the second location, people move easily between places. I knew this instinctively from all of my time traveling between the east coast and the west coast from Denver. When I went west, it was easy. When I went east, it was hard.

Magic trick number two is well-implemented video conferencing. I learned an approach many years ago from my now-partner Chris Moody that he used at Aquent when he was COO. He set up video conferencing in a cubical at each location at left it on all the time. Today, we have the equivalent on our desktops, so the cubical trick isn’t needed, but easy ways to immediately start video conferences at any time, as a substitute for in-person meetings, without having to go into separate rooms in the office, makes a huge difference in interpersonal interactions.

It seems pretty clear that a very large, single location company in Silicon Valley, New York, Seattle, and several other cities (e.g. LA, Boston) is getting much more challenging. Sure, it’s possible, but is it advisable?

I received plenty of useful feedback on my rant Budgets – There Has To Be A Better Way.

Two of the links that I found particularly helpful were:

- Turn Your Budgeting Process Upside Down by Robert Howell

- How to Ruin Your Company with One Bad Process by Ben Horowitz

Robert Howell points to a longer term view than one year with his suggestion around rolling plans. He also emphasizes a focus on economic value – specifically future cash flows – rather than accounting earnings. Simply – focus on cash, rather than non-cash calculations. He ends with a great paragraph on eliminating the word “budget” and reorienting it around your specific goal (e.g. “profit plan”, or “break-even plan”, or “maximum monthly investment of $500k plan.”)

Ben Horowitz describes how his budgeting process almost bankrupted his company LoudCloud, and how he now suggests a different approach based on constraints. It’s especially relevant for fast-growing companies. His approach is summarized below.

- Run rate increase – Note that I say “run rate increase” and not “spend increase”. You should set a limit on the amount by which you are willing to increase what you are spending in the last month of the coming year vs. the previous year.

- Earnings/Loss – If you have revenue, another great constraint is your targeted earnings or loss for the year.

- Engineering growth rate – Unless you are making an acquisition and running it separately or sub-dividing engineering in some novel way, you should strive not to more than double a monolithic engineering organization in a 12-month period.

- Ratio of engineering to other functions – Once you have constrained engineering, then you can set ratios between engineering and other functions to constrain them as well.

Then:

- Take the constrained number that you created and reduce it by 10-25% to give yourself room for expansion, if necessary.

- Divide the budget created above in the ratios that you believe are appropriate across the team.

- Communicate the budgets to the team.

- Run your goal-setting exercise and encourage your managers to demonstrate their skill by achieving great things within their budgets.

- If you believe that more can legitimately be achieved in a group with more money, then allocate that manager extra budget out of the slush fund you created with the 10-25%.

I love the theory of constraints as an operating principle for many things, and Ben applies it really well in his post.

Both articles are worth a detailed read – they are each short, but full of goodness.

I wonder if it means anything that each of the author’s last names starts with the letter H?

“This budget will let us have 2020 vision.”

I heard that quote at the end of a board meeting yesterday and laughed out loud. As someone with terrible eyesight (I’ve worn glasses since age 3 and had eye surgery at age 8), my “vision” has always been suspect …

I’m in Seattle for a few days doing the end of year board meeting/budget drill at a number of our Seattle-based companies and thought this was a priceless pun.

The person who said it also had complete awareness that the budget isn’t a prediction of what is actually going to happen in 2020, which made the statement even more clever.

I made sure to wipe off the lenses of my glasses before my next meeting to try to see a little better. By the time I got back to the hotel room at the end of the day, they were once again dirty and covered with dried raindrops.

We are in the middle of the budget planning process at many companies. This is a recurring Q4 event that spills over into Q1. Budgets for the next year (2020) get finalized between December 2019 and February 2020.

As I was daydreaming the other day during a budget discussion, I thought to myself “there has to be a better way.”

Since I started investing in private companies 25 years ago, I’ve been experiencing the same cycle over and over again.

The normal situation is end of year budget planning. Q1 performance on plan. Q2 performance slightly different from plan. Q3 and Q4 performance divergent from plan.

Occasionally companies completely miss their Q1 plan. I’ve always viewed the Q1 plan as a competency test – if you can’t make your Q1 plan, something fundamental is wrong with the business. Of course, when you blow your Q1 budget, the plan goes out the window and gets redone.

Occasionally companies far exceed their budget in Q1 or Q2 or find themselves on a positive trendline that has nothing to do with the original budget. Or, the opposite.

The budgets also have huge variability after financings, when suddenly the budget gets recast given the new money in the bank, or the constraints against hiring are removed and costs increase suddenly, even if this is only to “catch up” with the budget that was underhired to.

It’s all lagging indicators anyway when looking at performance to budget. By the time the November financials are reported, we are already deep into December, and that assumes there is a robust discussion around the monthly company performance.

Some companies are excellent at managing this process. Most are not.

I know of a few very companies, including one very large one (Koch Industries), that famously run without budgets. I’ve tried lots of small incremental things over the years, such as 1H, 2H budgets (running on a six-month budgeting process) and having an expense only budget that lags revenue by a quarter, but I’ve never really landed on something that (a) works, (b) is materially easier, and that (c) management accepts.

When you add up all the time spent on budgeting across all the organizations on the planet (including government), the human species wastes an enormous amount of time on a thing we don’t do very well.

There must be a better way.