Several years ago, I wrote a post titled Why VCs Should Recycle Their Management Fees.

From the start of Foundry Group in 2007, we have felt strongly about this. We feel that if an LP gives us a $1 to invest, we should invest at least that $1, not $0.85 (the average fee load over a decade for a typical VC fund is 15%.) Our goal for each fund is actually to invest closer to 110%, which means if an LP gives us a $1 to invest, we are actually investing $1.10.

Our long-time friends and LPs at Greenspring recently wrote a great post titled Creating GP-LP Alignment: Why Terms Matter. The post specifically discussed three items: Management Fees, Recycling, and Carried Interest.

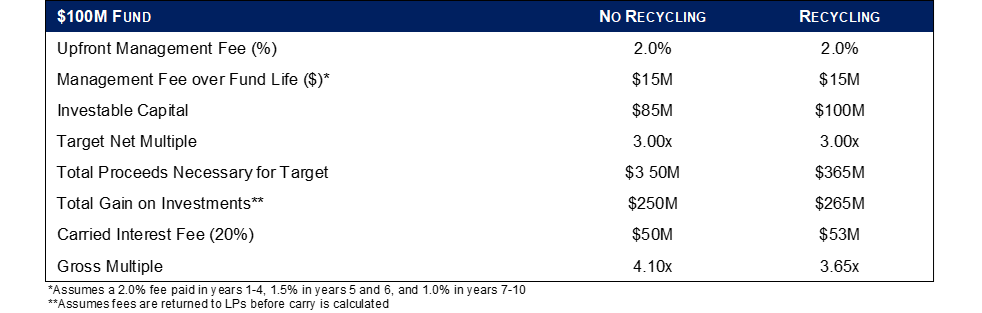

The entire post is worth reading, but I especially liked their section on Recycling which includes a handy chart showing that recycling means that you only need to generate a 3.65x gross multiple to achieve a 3.00x net multiple to your LPs, vs. a 4.10x gross multiple if you don’t recycle. The section from their post follows:

In addition to management fees, the process of reinvesting realized proceeds into new investments, or recycling, can also meaningfully impact net returns and alignment. While management fees cut into the dollars available for investment, recycling can have the opposite effect, increasing the investable pool of capital while offsetting a proportion of management fees. To illustrate this point, we revisit our $100 million fund example, and in this case show how recycling $15 million, equivalent to the fund’s management fee, positively impacts the fund.

The fund that chooses to recycle fees requires a 3.65x gross multiple to achieve a 3.00x net multiple, whereas the fund that does not recycle proceeds to offset management fees requires a 4.10x gross multiple to achieve a 3.00x target net multiple. As long as re-invested capital is prudently deployed into opportunities capable of generating strong results, recycling is an impactful way for GPs to increase net returns, which ultimately benefits investors and themselves.

Now, imagine if you recycled 110%. Your investable capital would be $110m. You now require a 3.45x gross multiple to achieve a 3.00x multiple. Plus, as a bonus, you get $56m of carry (vs. $50m of carry in the case where you don’t recycle proceeds.)

Many fund agreements, including ours, require us to pay back all fees and expenses before taking carried interest. We think this is another element of GP-LP alignment and have supported this from our first fund. As a result, if you recycle at least 100%, it is more realistic to think of your management fee as a risk-free, interest-free loan against future carried interest, instead of additional compensation.

As a result, our goal is to generate as much of a return on the dollars invested, and get as many dollars invested as we can in each fund. Recycling allows us to do this and brings the gross and net returns closer together, reducing the spread to the carried interest from profits on investments.

While many GPs focus on their gross numbers, in the end the only numbers that really matter to LPs over time are the net multiples.

That’s worth remembering.