Category: Term Sheet

When we were last with our SayAhh cofounders, they had implemented an accounting system and Jane had contributed $50,000 for a 55/45% equity split. This week we introduce two of SayAhh’s key accounting documents: the Balance Sheet (BS) and Statement of Cash Flows (SCF) showing how this investment is accounted for.

The investments by the founders created two transactions. Since SayAhh is a C corporation that is incorporated in Delaware, they decided to have a very low non-zero par value for their shares, set at $0.00001, to prevent higher franchise stock taxes. Thus for the 10M shares issued to the them, Jane invests $55 and Dick invests $45. Jane also invests $50,000 as previously agreed. These deposits increase the checking account balance and also the equity accounts, and results in a solvent company and a decent starting bank balance.

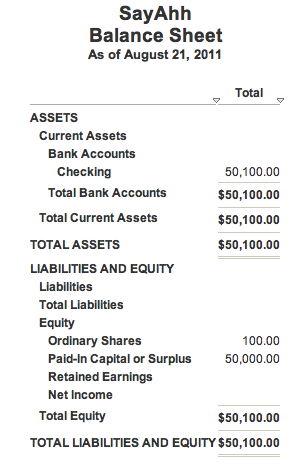

Below is the Balance Sheet as of 8/21/11. Fred Wilson’s MBA Mondays series shows how to think about the balance sheet – namely as a picture of the company at a point in time.

The Balance Sheet respects something called the Basic Accounting Equation. The Basic Accounting Equation states that Total Assets always must equal Total Liabilities plus Equity. In SayAhh’s case, you can see that the assets (cash in a checking account) equals liabilities (zero) plus equity. Assets = Liabilities + Equity.

If you use spreadsheets to keep track of your books, you could accidentally violate the Basic Accounting Equation, but not in accounting software program. This is one of the reasons that Dick and Jane chose to use QuickBooks, even at this very early stage, as it guarantees that their books will conform to double entry accounting.

Equity is comprised of two things. The Ordinary Shares equity account represent the par value paid by Jane and Dick for their 10M shares ($100). The Paid-In Capital account shows Jane paid in an additional $50,000. Combined these two amounts equal total equity, or $50,100.

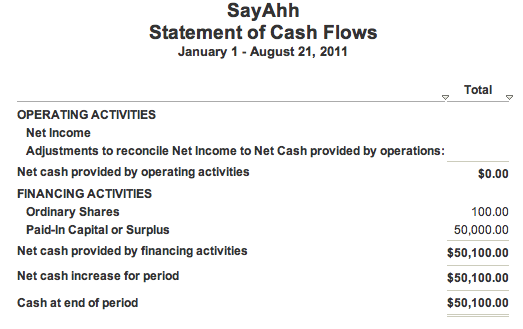

The other accounting document we are introducing today is the Statement of Cash Flows (SCF). The SCF breaks down how changes in balance sheet accounts and income affect cash. When presented in the SCF, these transactions are broken down into three categories: operating, financing and investing activities. Note the interconnected nature between these statements. The net $50,100 from financing activities all went into equity on the Balance Sheet.

Currently, SayAhh’s financials are very straightforward – even boring, but we’ve got to start somewhere. Next week we will introduce the Cap Table, and show how it changes when adding a co-founder.

When we were last with Dick and Jane on Finance Fridays, our fearless entrepreneurs were figuring out how to split up their founders equity and account for an investment from Jane. While they’ve been hard at work on their product, they’ve also incorporated the company, now named SayAhh (thanks Mac!) as a C-Corp in Delaware. They’ve done a bunch of other mundane things, such as establishing a business checking account and depositing Jane’s $50k in seed capital, but like all good early stage entrepreneurs, they’ve spent most of their time obsessing about their product, talking to a few potential early customers about what they needed, and coding away on their MVP.

Dick and Jane had limited formal business accounting experience, but they both knew how to balance a checkbook. They reached out to their friend John, a CFO at a late-stage VC-backed company in Boston that was about to file an S-1 to go public. John took an hour out of his day to do a conference call with Dick and gave them advice on how to set up their accounting system. His advice included the following,

- Set up a double-entry accounting system and use it to track all financial transactions.

- Build a financial model that forecasts the P&L. Revenues and costs should both be based off of a robust set of assumptions. This should tie to your GL for “Actuals” (i.e. historical data).

- Be sure to use accrual accounting, not cash accounting.

- Tie the P&L forecast to the Balance Sheet and Cash Flow Statement and generate snapshots of what the Financial Statements will look like each year for the next 5 years. Create monthly snapshots on a rolling 12 month basis.

- Anytime the financial model indicates that SayAhh will run out of cash, determine how you will raise capital to ensure liquidity and be sure to properly account for the debt or equity transaction on the balance sheet and Cap Table.

- Tie each round of funding to a set of key milestones in the development of your product/business.

John also mentioned a bunch of other stuff that Dick didn’t write down because they weren’t really sure what it meant, but it included phrases like 409a and VSOE. Feeling overwhelmed, Dick emailed his friend Josh, the CEO of an early-stage startup in Boulder, to see how they figured out all of this stuff. He summarized Dick’s advice and Josh replied: “That’s great advice and you should do all of that stuff – eventually. But, for now, focus on the following:”

- Make sure you both have business credit/debit cards and that you use them (or checks) for all transactions.

- Setup a simple accounting system like QuickBooks and sync it with your bank account. At the end of each week, make sure you’ve properly labeled each transaction using the QuickBooks Chart of Accounts. This takes a little getting used to, but you’ll pick it up. Ask me if you have questions.

- QuickBooks allows you to forecast expenses. Think through all of the expenses that you anticipate over the next 12 months and enter them. Update this every time you become aware of new transactions and maintain this on a rolling basis. QuickBooks will show you if/when you will run out of cash within the next 12 months.

- Build a plan as to how you will inject more cash into the business any time QuickBooks shows you running out of cash, and be sure to start raising any needed cash well in advance.

Dick and Jane followed Josh’s advice. It required a small investment of time and money to get QuickBooks up and running, but it was a manageable distraction from building SayAhh’s core product.

To be successful, you need to know about a wide range of issues affecting your business. However, you do not have to become an expert on each and the degree to which you need to understand various issues evolves along with your business. It is easy to get caught up in all the administrivia of of forming a company, building a business plan, and developing financial forecasts that you fail to spend time building your product.

How do you know what matters most when? This is where developing a network of trusted and qualified mentors comes in handy. While John was trying to be helpful, his advice missed the mark because he didn’t have a lot of experience at the early stages. In contrast, Josh was an experienced entrepreneur who had started several companies and likely learned his lessons through experience. As you build your business, surround yourself with as many Josh’s as you can. And, as you grow, make sure you find mentors like John to help you at at the appropriate stages.

As Josh suggested, when you first start your business you should focus on building systems and processes that allow you to accurately capture as much data as possible from the start. QuickBooks and other accounting software programs will do this for your finances, but you should also implement tools for tracking other key metrics (e.g. customer behavior, support inquiries, marketing analytics). You can and will become increasingly sophisticated in analyzing and interpreting that data over time, but you cannot analyze it if you do not have it.

Additionally, at all points in the development of your startup – including on Day 1 – you should focus intently on forecasting your cash flows as accurately as you possibly can. Running out of cash will either kill your company or force you into a very painful financing round. Know exactly when you run out of money, well before the time you hit a wall and go splat.

Finance Fridays: Getting Started – Allocating Equity and Founder’s Investment

Finance Friday’s gets off the ground with today’s post by introducing you to an imaginary startup, the entrepreneurs that we’ll being following throughout the series, and their first challenges: splitting up the founders’ equity and addressing the case where one of the founders provides the initial seed capital for the business.

We felt like we needed to put some groundwork in place using a case-study like approach, rather than just jumping into looking at balance sheets, income statements, and cash flow statements. Hopefully, by the time we are done, we’ll all have some new friends and a lot of knowledge. Let’s get started.

Jane and Dick worked together at Denver Health, the nation’s “most wired” hospital according to Hospitals & Health Networks Magazine. They have seen first-hand the impact technology can have in the medical field through exposure to a number of Denver Health IT initiatives. Through a series of conversations, Jane and Dick have come up with the idea to develop a social network tailored to the medical community. Through an online platform, doctors, nurses, and administrators would be able to assist each other with complicated diagnoses, collaborate on research studies, and find and fill job openings. After sharing the concept with a number of colleagues and receiving enthusiastic support for the idea, Jane and Dick built up the confidence to quit their day jobs and launch a business together.

Jane and Dick each brings a similar level of skill and capability to the business, making it easy for them to agree to a 50/50 equity split. While they could both go without salaries for a year, Dick had no extra money to invest in the business. However, Jane was in a position to invest some of her savings into the startup. How could they treat Jane’s cash investment in the business in a way that was fair to both of them?

Jane could have covered expenses from her personal account for now, keeping track of the receipts, with the plan of letting an accountant sort it out later. After all, they needed to focus on building their product, right?

Fortunately, Dick and Jane had both read Dharmesh Shah’s piece on avoiding co-founder conflict in Do More Faster and knew it was important to address co-founder issues – including how to handle co-founder investments – from the start. They also knew that it was important to set up proper accounting systems from the beginning and that paying for bills out of your personal bank account and having an accountant sort it out later for you seemed like a recipe for future pain.

Jane and Dick had several options, including structuring this as a debt transaction where Jane simply loaned the money to the company, or as convertible debt transaction where Jane’s investment would convert into equity in the next round. But they worried that future investors would frown on that or wouldn’t give Jane credit for the investment at a later date, since they might consider it as part of Jane’s contribution to her original ownership position of 50%.

That narrowed the possibilities down to an equity transaction, which would in turn require a conversation about valuation. Jane and Dick briefly considered a valuation based on the next external financing round, perhaps applying a discount. For example, if the first round of external investment values the company at $2 million post and, prior to that, Jane had invested $50,000, then with no discount, Jane’s investment would earn her 2.5% of the company ($50k/$2M = 2.5%). If they agreed on a 20% discount, then Jane would be entitled to 3.125% of the company ($2M * (1-20% discount) = $1.6M; $50k/$1.6M = 3.125%).

At this stage it wasn’t clear when (or even if) the first round of external financing might occur or what it might look like, which made agreeing on a discount just as difficult as agreeing on a valuation, while adding complexity. After a tense conversation about this, Jane and Dick decided to go out for a beer and try to resolve the equity allocation issue once and for all.

Jane indicated that the most she could invest in the company before they would have to seek other sources of capital was $50k. Dick hated to think that he would be diluted by more than 20% of his stake over $50k and proposed that Jane receive 10% incremental equity for her $50k. Jane felt comfortable with receiving 10% for $50k, but no less, so they agreed on a $450k pre money valuation of their startup.

There are a number of ways Jane and Dick could have executed the equity transaction. The simplest would be if they agreed in the founders documents that they would both commit full-time to the business, Jane would contribute an initial $50k, and they would split the equity 55/45 in favor of Jane.

Dick and Jane have now successfully navigated their first finance challenge: dividing up the founders’ equity, including an investment from one of the founders. A few key lessons from today’s post are:

- Invest the time upfront to get the founders’ documents right. This will save a lot of pain down the road. This includes agreeing on how you will handle personal investments in the business, but it also includes many other topics such as founders’ vesting schedules and voting rights.

- Every time you put money in the business it represents some form of debt or equity transaction. You can introduce complicated mechanisms for handling these transactions (e.g. warrants or discounts). However, there is a lot to be said for keeping things simple during the early stage of a startup. It helps control transaction costs in terms of both time and money.

- You could inject more cash into the business on an as-needed basis. However, this is distracting, even if you are raising the money from yourselves. Each cash injection effectively represents a new round of financing, which can get messy. Try to minimize the frequency of transactions by investing enough money each time to get you to the next key milestone for your business.

Next week, we will address how Jane and Dick put proper accounting systems in place. Oh, and you’ll notice that they don’t yet have a name for their company. They’ve told us they are open to suggestions.

Last week I expressed my frustration with the current lack of financial literacy that I see all around me. In the spirit of Fred Wilson’s awesome blog series MBA Mondays, I’ve decided to write a series of posts about this and asked for suggestions. I got a bunch, but one that stood out was from a group of incoming MBA students at the University of Chicago Booth. Their suggestion was to write a series of posts that follows the development of an imaginary startup as the company navigates various events, focusing on how each event will impact not only the P&L, but also the Balance Sheet and Cash Flow Statement.

I thought this was a great idea, so I engaged Jonathan, Simon, Kevin, and Kevin (you can meet them below) to help out. They are going to help me prepare the posts each week, which will include developing excel spreadsheets that we will upload to complement the posts. They suggested we call this “Finance Fridays” to bookend Fred’s MBA Monday’s – I checked with Fred to see if he was ok with this and his response was “Hell yes. The more the merrier.”

We would love to get your suggestions in the comments section for (1) the type of company that we should follow, and (2) the types of issues that the company might encounter (reminder: the goal is to illustrate common difficulties entrepreneurs face when it comes to understanding their financials). At this point we are planning to use a consumer Internet company as an example, but we are also considering using a SaaS-based software company.

As a special bonus for me, I get to work with four students on a project. I love working with and mentoring students, and am especially thrilled when they proactively reach out to me.

Our first substantive post will be up next Friday. In the mean time, please meet the Finance Fridays team:

Jonathan Wolter has been a lead consultant and software engineer at ThoughtWorks working for clients in Silicon Valley, Texas, Chicago, and India. Now he is slated to enter Booth at the University of Chicago in the fall. On the side, he started a company selling accounting training to landlords. Previously he was at FeedBurner, and has never met a side project he did not love.

Kevin O’Leary has spent the past year working as an independent financial consultant to start-ups in the healthcare, telecom and nonprofit industries on projects both domestically and internationally. Prior to that, he was an investment banking analyst in the Medical Devices group at Piper Jaffray. He will be entering Booth as an MBA Candidate this fall.

Simon Zhang spent three years as a financial and tax consultant at Deloitte Canada with a focus on businesses in mining, financial services and technology sectors. He is a Canadian Chartered Accountant. He also lectured an undergraduate tax course at Simon Fraser University and frequently facilitated professional education courses with Canadian Institute of Chartered Accountants. With a strong interest in entrepreneurship and technology, he subsequently joined a technology start up project at Orbis Investment Management Ltd, an asset management firm with over USD $25 billion under management. His focus was to incubate an internal start-up which is built on state-of-the-art technology, novel business model and innovative products. He will be entering Chicago Booth to complete this MBA with a focus on entrepreneurship and finance in the Fall 2011.

Kevin McCaffrey left his job as a strategy consultant in the Chicago office of McKinsey & Company to found Dot-to-Dot Children’s Books, a nonprofit social enterprise that works with children around the world to develop children’s books that are marketed to raise funding and awareness for the authors’ communities. Dot-to-Dot relies entirely on earned income and employs a unique cause-related marketing strategy designed to establish a successful position in the competitive children’s lit market. Kids from eight countries, including Cambodia, Eastern DR Congo, and Afghanistan, have participated in Dot-to-Dot projects. Kevin’s experience with Dot-to-Dot has him hooked on entrepreneurship, which will be his focus at Chicago Booth.

I’m stunned by the lack of financial literacy of so many people in so many contexts. The commentary by politicians, economists, and the media on the European debt crisis and the US debt ceiling dynamics is appalling. The general media and blogosphere commentary on the financials of high growth companies, especially those who have either recently gone public or filed their S-1’s, range from perplexing to just plain incorrect. And more and more entrepreneurs who I’m exposed to who are presenting their companies for financing have a complete lack of understanding of their financials – both current and projected. Of course, some of my fellow board members don’t understand how to read financial statements either, which doesn’t help matters much.

Fred Wilson took on some of this with his awesome MBA Mondays series, including several great posts around financial statements that every entrepreneur should go read right now:

In my experience there are four specific things that people struggle with.

- An inability to read the Balance Sheet, P&L, and Cash Flow statements.

- A lack of understanding of how the Balance Sheet, P&L, and Cash Flow statements fit together.

- A lack of understanding how non-accounting metrics (e.g. bookings) impact the financial statements.

- A lack of understanding of GAAP (Generally Accepted Accounting Principles) and how to use the financial statements to help normalize out all the weird things GAAP makes you do.

I used to think it was all a GAAP problem. GAAP is complicated, continuously evolving and changing, and often creates more ambiguity that it resolves. But unless you actually understand how to read a financial statement, GAAP doesn’t even come into play. And by financial statement, I don’t just mean the income statement (or P&L) – I mean the income statement, balance sheet, and cash flow statement, along with understanding how they interact with each other.

If you understand how to read the financial statements, then you can start to solve for the GAAP challenges. You’ll be able to understand things like the implications of deferred revenue on cash flow, stock option expense on net income, and the actual equity dynamics of the balance sheet.

While there are so many things about this that I fantasize about (e.g. “the media would actually learn this stuff” and “accountants would make GAAP simpler and clearer vs. more complex”) the only thing that really matters in my world is that entrepreneurs understand how to think about this stuff. So, in the spirit of Fred’s MBA Mondays series, I’m going to write a series of posts that describe how my brain processes the financial statements of a typical high growth company with a goal of adding on to the great base that Fred has created.

I’m open for suggestions as to whether I should take on one that is newly public (e.g. the S-1 and historical financials are available), or a private company (I’m open to volunteers, although it’ll mean you are publishing your financials – at least at this moment in time.) If you’ve got suggestions or want to volunteer, just leave a comment.

While some people hate the phrase “failing fast”, I find it instructive when it’s used to signify that one isn’t going to pursue a particular path in the context of a larger set of activities. A few weeks ago, I wrote a post about The Proliferation of Standardized Seed Financing Documents. It generated several hundred email responses and a handful of phone calls. A week or so later, my partner Jason Mendelson wrote a post titled Why There Will Never be a Standard Set of Seed Documents. I’ve concluded that Jason is right so rather than torture myself, I’m failing fast with regard to trying to help create a set of standardized seed documents.

Since I received so many private responses to the original post, I thought I’d summarize them here by type of respondent.

Lawyers: By far the largest numbers of responses were from lawyers offering to help (thanks!) I didn’t count them up, but I got well over 100 emails from all over the US. In many cases, the lawyer offered to come to the meeting, share their seed documentation, and work to make sure that seed documents were complete and acceptable to their firm. The vast majority of lawyers provided solid background on all the seed investment work they had done. Several weighed in with their views of the potential issues, often sighting the NVCA standard document process which everyone seemed to refer to as some version of “a mess.” A few made sure to remind me that east coast lawyers needed to be involved or the docs wouldn’t work on the east coast. A few brave ones told me why I was destined to fail but wished me luck anyway. Fortunately, due to the magic of Gist, I now have contact information for a whole bunch of lawyers I didn’t know before.

Entrepreneurs: The next largest number of respondents were entrepreneurs. I think all of them cheered me on, told me how much they hated paying lawyers for their seed documents, and asked if there was some way to reduce everything to a few standard pages, not unlike a mortgage document. A few told me “don’t include lawyer X in the process – he charged me $70,000 for my seed deal” and a few suggested that lawyers should have to use paper and crayons instead of word processors. Several asked if I’d be interested in funding their companies. All demonstrated a sense of humor about the situation.

VCs: The VC comments came in a few different flavors. A few said “I don’t see the problem – it’s fine having multiple seed documents.” Another reminded me that “great is the enemy of good” (although the real, and more relevant quote is “The perfect is the enemy of the good”) and the existing forms floating around are “very good – much better than they used to be.” Another suggested that none of the standard docs worked for him, but he was perfectly happy to sign the forms from Law Firm Z without any modification. Several asked me whether I was still watching 24 (yes, I will watch it to the bitter end.) I received private emails from each of my partners containing a slightly different version of “are you out of your fucking mind?”

LPs: I only had one email from an LP. It was a short one. “Don’t waste your time on this.”

After pondering all of this, I realized that I was both trying to solve a problem that didn’t really want to be solved while at the same time falling into a common trap of working on something that, while on the surface seems like a good idea, isn’t really my issue to solve, at least not in this way. As many of you know, the issue is not only the term sheet, but also the underlying documents supporting the deal. I think this is a nuance that is often missed, as the seed docs need to be robust enough to easily support a next round financing (Series A or Series B) since the seed financing is rarely the last one. So, while a simple term sheet might be able to be agreed on, I realized that getting the actual docs agreed on would be a miserable, and likely impossible, thing to try to deal with.

Hence my failing fast. While in theory this might be a great idea, I’ve concluded that I can’t be successful at this. There are plenty of people – namely all the lawyers that work with startups – that have a much greater incentive than I do to get this right, be efficient for the entrepreneurs they work with, and be cost-effective for the companies they bill. So, I’m going to leave it to them.

As of today’s announcement that Ted Wang at Fenwick & West has collaborated with a group of bay area early stage VC’s and angel investors to create the Series Seed Documents we now have – at my count – four different standardized seed financing documents floating around the industry.

- TechStars Model Seed Funding Documents (by Cooley)

- Y Combinator Series AA Equity Financing Documents (by WSGR)

- Founders Institute Plain Preferred Term Sheet (by WSGR)

- Series Seed Financing Documents (by Fenwick & West)

Many smart and capable people have either worked on these various docs on signed on as supporters. However, until there is one standardized set of documents that everyone – especially the various law firms agree on – I don’t expect there to really be a standardized set of seed financing documents. I wrote about this in my post The Challenge of The Ideal First Round Term Sheet.

Rather than whine about it, after reading the PEHub article Marc Andreessen on “Series Seed Documents,” and Why VCs Should Start Using Them I’ve decided to try to get a handful of lawyers in a room and try to come out with one set of documents. This might be a futile effort, which will prove the point that it’s impossible to create one standard set of documents. But – I’m an optimist, so I’m going to plan for a good outcome.

I’ll proactively reaching out to the appropriate folks at Cooley, WSGR, and Fenwick & West to organize a one day session, with laptops, somewhere in the bay area. I’ll include a handful of early stage investors (both VCs and angels) in this effort. My goal will be to finish the day with a truly standardized set of seed documents that all of the firms agree to use. Then we’ll open source these and evangelize them across the startup world, at least in the US.

If you are an attorney at a major national or regional law firm that works with startup companies, please email me if you are interested in participating. If you are a VC or angel investor that supports this effort – same drill (email me). Let’s end this madness (which I’ve been dealing with for 16 years and an angel and VC investor) once and for all – the entrepreneurs who we work with deserve better from us.

Over the years my partner Jason Mendelson and I have heard from numerous people that they’ve been exposed to our Venture Capital Term Sheet Series as reference material in a college course. We are delighted by this and whenever we’ve been asked, we’ve always said (and will continue to always say) “with our blessing.” However, we haven’t kept track of any of this over the year and have a few ideas for things we can do to update the material now that five years have passed.

So – I’m writing with a simple request. If you’ve used, or encountered, our Term Sheet series in a college (undergraduate or graduate) course or any other teaching / seminar environment, can you leave a comment below with the information (school / program / year / professor) or email me the information?

For those of you concerned about nefarious plots on our part, I assure you that we are delighted this material is out there in the public and are happy to have it freely used and passed around for all eternity. I promise we won’t send Jack Bauer your way.

We are deep in budget season as the last board meeting of the year typically includes the 2010 Budget – or at least the “2010 Draft Budget” or “2010 Budget – Draft”. This is also known as “the joy of cramming a spreadsheet into a powerpoint presentation.”

The budgets I see generally fit into one of the following five categories.

- Pre-Revenue: We are pre-revenue and won’t generate revenue in 2010.

- First Year of Revenue: We are pre-revenue but will generate our first revenue in 2010.

- Growing Revenue: We are on a revenue growth curve in 2010 but will lose money every month.

- Becoming Profitable: We are currently losing money but will become profitable in 2010.

- Profitable: We are profitable every month this year.

While I’ve written about this before, it’s worth noting that “profitable” is often used to mean either EBITDA positive, Net Income positive, or Cash Flow positive. These are three totally different things and you aren’t really in a happy profitable place until all three are true.

Of the five types of budget categories above, three (#2, #3, and #4) typically have the “hockey stick problems.” Specifically, the revenue curve in the budget model looks like a hockey stick throughout the year with steep revenue growth in Q3 and Q4.

The hockey stick revenue helps justify additional head count and an overall ramp in expenses. If the revenue plan is correct, this is fine. But the revenue plan is rarely correct, especially in Q3 and Q4. As a result, the expense base in the budget is much too high. One of two things happen – the budget breaks (and gets ignored) or the company continues to operate on the expense budget (or some approximation of it), resulting in a much bigger loss and cash spend than forecasted at the beginning of the year.

There’s another issue – hiring is often front end loaded and the timing is somewhat unpredictable. It’s also hard to “unhire” a month after you’ve hired someone because you are below budget. While some people talk about people as a “variable cost”, it’s a tough variable cost to immediately turn to zero shortly after you’ve hired someone.

Each case is a little different, so let me spend some time on how I think about each one.

First Year of Revenue (#2): The problem in this case is that the company will burn through its capital faster than expected. You can solve for this by forcing the expense budget to look like a pre-revenue budget (e.g. assume no revenue). When revenue starts to ramp, then you rebudget, even if it’s mid-year. Basically, discount all revenue to zero until you start generating it.

Growing Revenue (#3): This is the trickiest of the three cases. You have revenue. You want to spend more money to grow revenue (this is rational). You expect revenue will grow nicely (maybe, maybe not). In this case, I suggest you build the budget and then shift your expense plan forward by one quarter. This delays the spending ramp by 90 days which enables you to see if you are ramping revenue as expected. I’ve rarely seen this slow down the revenue growth and, when it’s clear that revenue is ramping ahead of plan, you can always layer in some expenses explicitly ahead of plan.

Become Profitable (#4): Similar to #3, you start by lagging your expense ramp by a quarter. Equally important, you should manage to a net cash number (cash + borrowing capacity – debt) and make sure you never fall below a threshold that is set as part of the budget process. Once you start generating positive cash flow, you can rebudget, just like case #2.

I find that Pre-Revenue and Profitable companies typically don’t have the hockey stick problem in the budgets. Pre-Revenue don’t by definition since they have no revenue! Profitable companies have usually been through the cycle so many times that (a) they understand how to be realistic about revenue growth and (b) they are so happy to be profitable and self-sufficient that they err on the side of under-budgeting revenue and then expanding their expense base as they exceed plan.

Be smart – avoid the hockey stick. Even when you are playing hockey! It hurts when it hits you in unexpected places.