When we were last with our SayAhh cofounders, they had implemented an accounting system and Jane had contributed $50,000 for a 55/45% equity split. This week we introduce two of SayAhh’s key accounting documents: the Balance Sheet (BS) and Statement of Cash Flows (SCF) showing how this investment is accounted for.

The investments by the founders created two transactions. Since SayAhh is a C corporation that is incorporated in Delaware, they decided to have a very low non-zero par value for their shares, set at $0.00001, to prevent higher franchise stock taxes. Thus for the 10M shares issued to the them, Jane invests $55 and Dick invests $45. Jane also invests $50,000 as previously agreed. These deposits increase the checking account balance and also the equity accounts, and results in a solvent company and a decent starting bank balance.

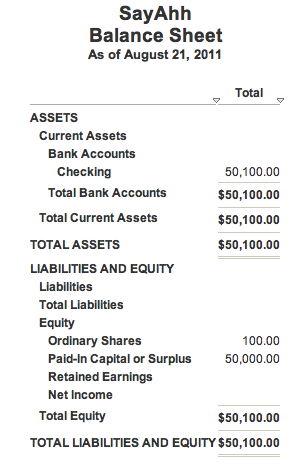

Below is the Balance Sheet as of 8/21/11. Fred Wilson’s MBA Mondays series shows how to think about the balance sheet – namely as a picture of the company at a point in time.

The Balance Sheet respects something called the Basic Accounting Equation. The Basic Accounting Equation states that Total Assets always must equal Total Liabilities plus Equity. In SayAhh’s case, you can see that the assets (cash in a checking account) equals liabilities (zero) plus equity. Assets = Liabilities + Equity.

If you use spreadsheets to keep track of your books, you could accidentally violate the Basic Accounting Equation, but not in accounting software program. This is one of the reasons that Dick and Jane chose to use QuickBooks, even at this very early stage, as it guarantees that their books will conform to double entry accounting.

Equity is comprised of two things. The Ordinary Shares equity account represent the par value paid by Jane and Dick for their 10M shares ($100). The Paid-In Capital account shows Jane paid in an additional $50,000. Combined these two amounts equal total equity, or $50,100.

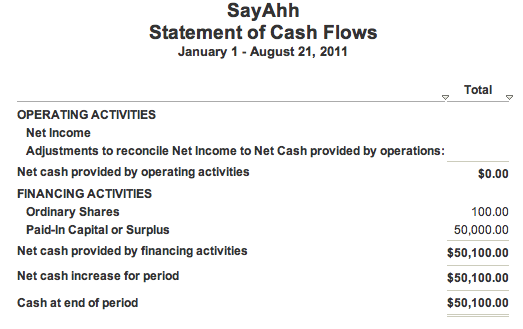

The other accounting document we are introducing today is the Statement of Cash Flows (SCF). The SCF breaks down how changes in balance sheet accounts and income affect cash. When presented in the SCF, these transactions are broken down into three categories: operating, financing and investing activities. Note the interconnected nature between these statements. The net $50,100 from financing activities all went into equity on the Balance Sheet.

Currently, SayAhh’s financials are very straightforward – even boring, but we’ve got to start somewhere. Next week we will introduce the Cap Table, and show how it changes when adding a co-founder.